have you run curvesim to determine optimal pool params for the pool? I suggest backing this change with some analysis first if you haven’t already and llamarisk can help with this if you like

This vote has already passed with the proposed parameter changes, but for Usual’s reference and for benefit of other protocol’s interested in further optimizations to their pools, we give our analysis here.

Motivation

We understand the proposal to be motivated by the following points:

to have enough redemption liquidity towards the reference asset.

absorbing redemption volatility during Usual Money launch.

securing deeply liquid secondary markets during US off-banking hours.

Usual.money plans to onboard more avenues of redemption, but those deals take time to materialize, so the curve pool acts as the secondary market that needs to be tended to until those market structures are up in place.

Therefore our primary motivation is to ensure maximal liquidity density in all expected conditions based on the historical pool behavior.

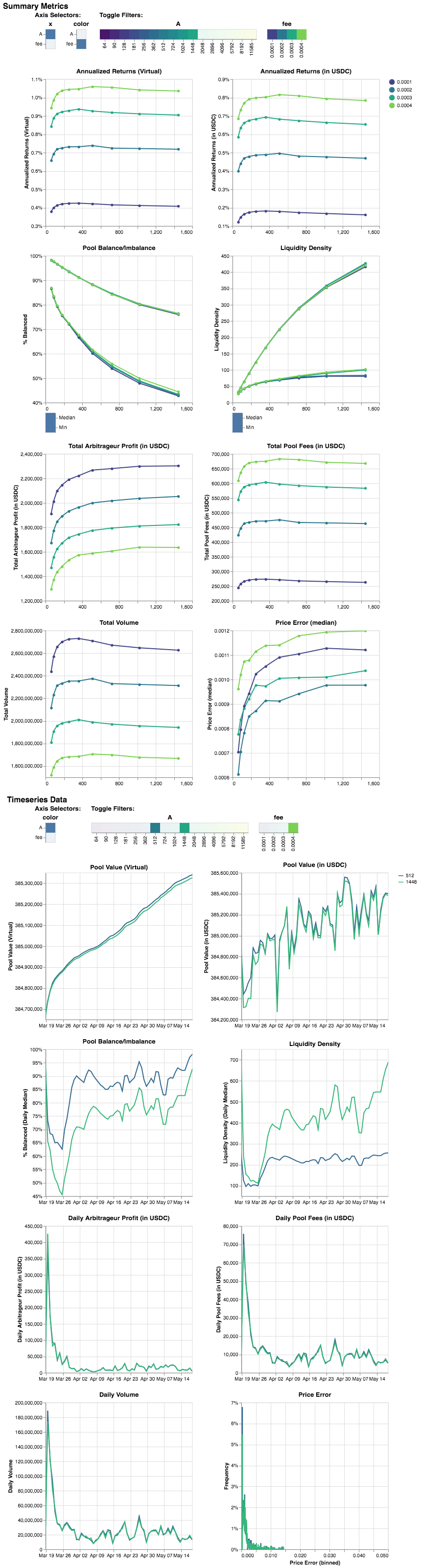

Simulation Analysis

Our simulation results suggest that an A value of 512 optimizes overall pool returns while maintaining a good balance. However, the proposed A of 1000+ does indeed improve liquidity density significantly, at the cost of potentially increased price errors and slightly lower overall returns

The interplay between the offpeg multiplier and pool fee is particularly interesting for this type of pools. In stable conditions, a lower base fee of 0.02% could attract more volume, potentially increasing total fee revenue if the volume increase outweighs the fee reduction. According to simulations, arbitrage-only volume would increase ~39% by reducing the fee from 0.04% to 0.02% and overall pool fees would reduce 30%. During depeg events, the higher offpeg multiplier of 5x becomes critical, however, which should partially offset the reduction in fee revenue.

Considering these factors, we agree that a strategy of lower fees and higher multiplier can satisfy the intent of this proposal. It aligns with Usual’s goals and likely optimizes long-term returns while maintaining competitiveness. However, we offer a slightly amended recommendation that seeks to improve liquidity depth while having less impact on pool revenue:

Fee: 0.03% - 0.035%

Offpeg multiplier: 3x

A: 750

This proposal should achieve the desired liquidity density improvement while incorporating insights from our simulations. The min pool balance is expected to be ~55% at A = 750 vs around 50% at A = 1000. This strengthens the pool’s assurance to have redemption liquidity available while reducing the slippage that users may experience upon redemption.