Proposal to raise A parameter on DOLA pool from 100 to 450

Abstract:

Increasing the A factor will reduce slippage for LPs doing large deposits and withdrawals, as well as encourage larger trades. Simulations show that this parameter change is the optimal value for maximized returns for both LPs and the DAO.

Raise the A parameter from 100 to 450 on the DOLA pool

For:

Increasing A parameter will decrease the volatility of DOLA’s peg due to large LPs moving funds and large trades. Increasing the resilience and stability of DOLA’s peg is essential for its utility as a stablecoin.

Against:

Do not raise the A parameter of the DOLA pool (do nothing)

What is the plan to stabilize this?

Would be good to get a clear system healthy matrix or be open about that?

Was reading in your discord: Discord

“As long as CRV rewards continue, this should be plenty enough in order to protect the peg …”

This kinda wishful thinking is not proper risk management.

If there is a depeg or any stress on the system it is better to keep the A parameter low for it to recover faster IMO

I’m concerned at the wording of forum post for the “for” vote:

Increasing A parameter will decrease the volatility of DOLA’s peg due to large LPs moving funds and large trades. Increasing the resilience and stability of DOLA’s peg is essential for its utility as a stablecoin.

Yes, “increasing the resilience and stability of DOLA’s peg” is crucial, but that is not a stableswap pool’s proper role. All increasing A really does is increase the leverage of the bet LPs are making, allowing them to win with greater pool imbalance but with greater losses when wrong.

If the DOLA peg becomes unsound, this increases LP risk and large emissions will not stop risk-averse LPs from fleeing a depeg, which can readily happen in a day. The wording suggest to me that there is a misunderstanding of the role of the A parameter in this basic risk-reward tradeoff.

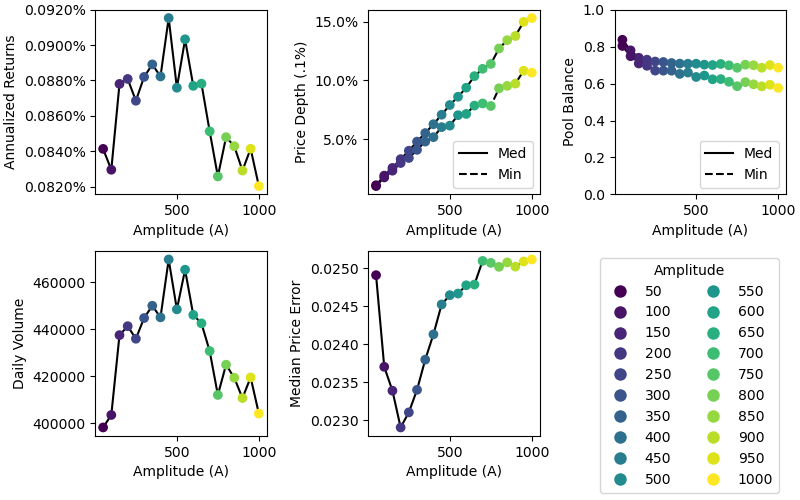

Proposing to raise A to 450 also overlooks this tradeoff in another way. While it’s true that 450 achieves the max in the returns graph, the graph is quite noisy there. Raising to 500 drops the returns to comparable levels to A = 150 but A = 550 magically brings returns back near the peak. It is prudent to maintain a margin of safety with the understanding that higher A is more risk to LPs.

The returns for A = 150 are quite similar to those of much higher values with median price error considerably lower. This suggests the higher A results are running into sim limitations. Based on all this, it would be wise to keep A low; possibly raising to 150 is ok.

DOLA currently carries $9.5MM in bad debt as a result of two price oracle incidents that occurred in Q2. The risk dao figure includes all bad debt (DOLA, ETH, wBTC, YFI) on our lending market, however for this topic it’s most appropriate to focus on just DOLA, which is around $9.51MM.

The way Inverse raises and lowers rates across lending markets is referred to as the “DOLA Fed” model which is fairly unique among stablecoins. DOLA is a fully-recallable, debt-based stable, meaning we are free to act to raise interest rates in lending markets, as we have previously to maintain the peg. In the case of DOLA-3POOL, we currently manage the DOLA Fed in close collaboration with our partner, Yearn. We currently control the expansion and contraction of DOLA through the “Yearn Fed”, which mints and burns DOLA directly to and from the DOLA-3Pool. An example of how effective this is at controlling the peg was on June 16th when $24.5MM of DOLA was burnt from supply in a single transaction: https://etherscan.io/tx/0x24d32a894d2436e63a47db21425d466737de5ff3708322648fd628274d9f66d6

We’re executing weekly repayments and have earmarked future revenue (e.g. doing our own liquidations) from future products for this purpose. Currently, the majority of these repayments are funded by selling bonds (via Olympus Pro). See our bond stats here.

The Discord reference to the role of CRV rewards in defending the peg was intended to informally illustrate that we are able to defend the peg by incentivizing LP’s. This is true whether on Curve or on other platforms like Velodrome or Balancer where we are expanding DOLA liquidity. Regardless, we believe the expectation that Curve emissions will continue is reasonable due to our plans for future “bribes” to veCRV and vlCVX token holders and accumulation of vlCVX.

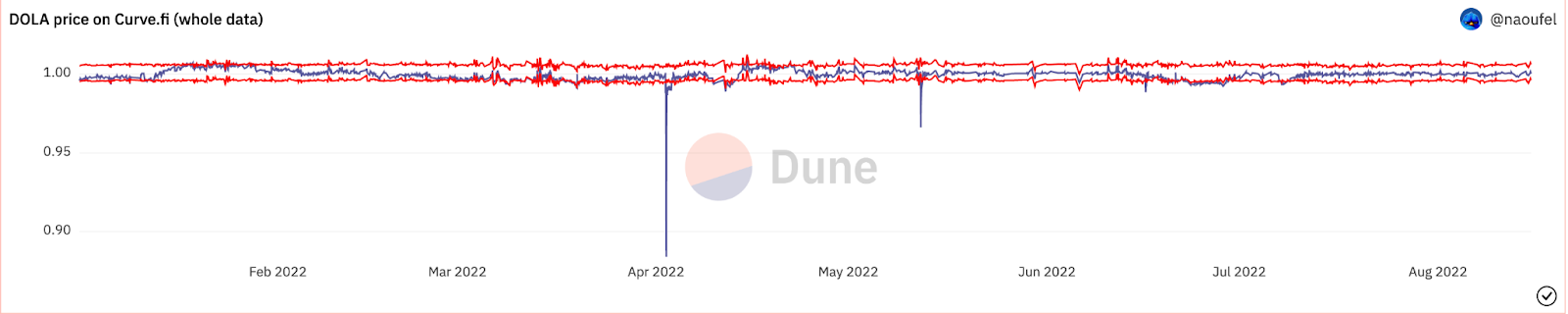

Agreed. This is as true for DOLA as it is for any other stablecoin on Curve, so we do not believe this to be a determinant in capping the A parameter of DOLA. DOLA’s Fed mechanics have proven to be highly resilient at defending the peg, even during times of extreme stress. The DOLA-3Pool experienced 3Pool bank runs twice (on the days of oracle exploits) on April 2nd and June 16th; both times DOLA depegged for very short periods of time. Please see our graph below of DOLA’s peg YTD:

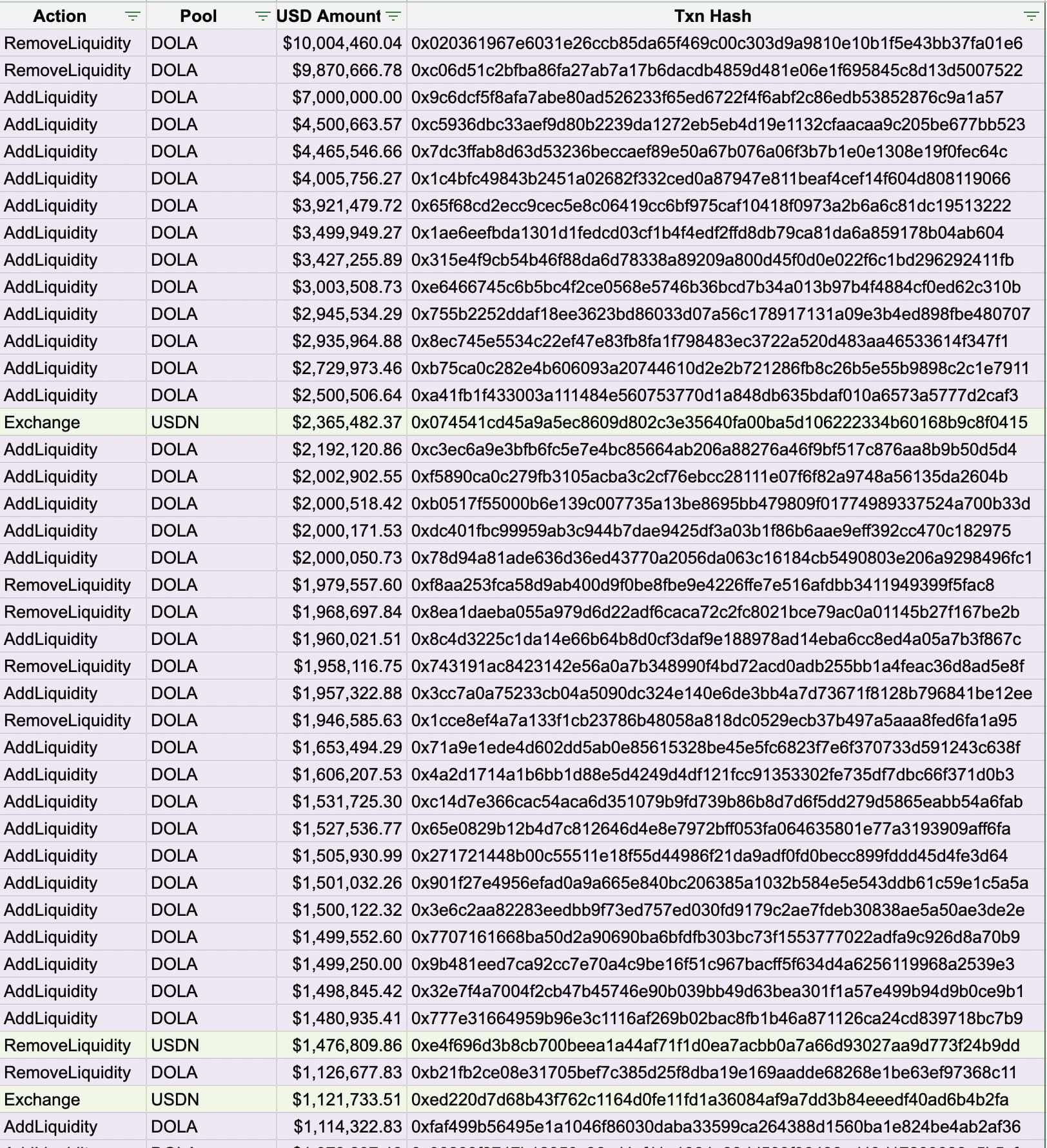

The A param does not increase or decrease the risk for LP’s, it only makes the timing of entry and exit more sensitive as it increases. Large wallets (DAOs/funds/whales) are reaching out to us and letting us know that they would prefer to do larger, single transactions in DOLA-3POOL but they are currently prevented from doing so due to slippage. By increasing the A param, we allow these users more certainty of pricing outcome by reducing slippage. The same holds true for large depositors wanting to exit the pool more gracefully. Here’s a recent example of a large wallet exiting and incurring over ~$7k in slippage losses despite the pool being very well balanced at the time of transaction.

Regarding the peg, re-pegging is difficult when the only incentive is a peg discount (e.g. MIM before it started switching to variable rates). DOLA addresses this by having multiple battle-tested peg control mechanisms. When needed we rely on variable rates to penalize shorts by raising rates. We’re able to force shorts to repay during an imbalance or face an ever-increasing borrowing cost. Most notably, we are able to contract the Curve LP via our Yearn Fed, which is the largest pool depositor. This mechanism is instant and does not rely on the behavior of any other market participants or mechanics. Here is an example of a $10m contraction that was done to rebalance the DOLA-3Pool after the example from the previous paragraph.

However, we are in agreement with you that the “increasing the resilience and stability of DOLA’s peg” phrasing, while important, is not a stableswap pool’s proper role. The OP is not able to be edited, but we retract that sentence from the “FOR” section.

Looking at Annualized Returns and Median Price Error graphs, A param values of 150 and of 300 yield the same results (~0.088% for annualized returns, ~0.0237 for median price error). A param of 450 has the highest annualized returns (0.092%) with median price error only ~3.3% higher (0.0245 vs 0.0237). An A param of 450 will also result in the highest volumes as shown in the simulations by @nagaking. This is crucial for Inverse as we pursue a Chainlink price oracle for DOLA which comes with volume, as well as pool depth requirements. We believe a DOLA Chainlink price feed will ultimately greatly benefit the DOLA ecosystem, including LPs in the DOLA-3Pool.

This analysis is beyond my paygrade, but I do agree with @edo that we want to lock in integration with Chainlink (the sooner the better); and to do that DOLA needs to incentivize and attract larger LPs.

Looking at the charts provided by @cryptoharry, 450 seems to strike a balance: at the peak of Annualized returns and Daily Volume, and in the median for the rest.

I translate this as a moderate increase to risk, relative to a great increase in returns. Given the state of the market, and the attractiveness of stablecoins LPs at the moment, this could be a killer move at the right time.

Finally, the $10 mil in bad debt has been addressed. It is old news, and not relevant to this topic except that it is one more thing holding DOLA back from achieving a major break through in Total Liquidity and volume.

Happy to run this same comparison on other Curve pools as well if there are suggestions.

In the meantime, I would like to voice my support for an increase in the DOLA pool A parameter to 450.

At the end of the day, the only thing that matters is whether (and/or to what extent) DOLA can be redeemed for its underlying at the expected value (~$1). We need clarification: can it be? Can all of it be?

If not, it is inappropriate (or at least unwise) to ask LPs to lever up their bet that it can be. Raising A is directly analogous to levering up on a bet of 1:1 parity. It is incorrect to say that LPs do not incur additional risk when A is raised. For example, with higher A, LPs suffer more impermanent loss upon depeg.

Finally, as the author of the above research, I want to clarify that it is only as accurate as the data it was run on (last 2 months price data). If there is strong reason to believe that data is not representative of future price dynamics, the result is entirely void.

In my opinion, if the coin is not fully backed, there is no reason to expect that such price stability will continue, rendering the simulation essentially meaningless.

The A param does not increase or decrease the risk for LP’s…

No, you are simply wrong here. There is no free lunch. Someone has to bear the cost for the benefits going to traders. The cost is carried as risk by LPs.

However, we are in agreement with you that the “increasing the resilience and stability of DOLA’s peg” phrasing, while important, is not a stableswap pool’s proper role. The OP is not able to be edited, but we retract that sentence from the “FOR” section.

Great!

Looking at Annualized Returns and Median Price Error graphs, A param values of 150 and of 300 yield the same results (~0.088% for annualized returns, ~0.0237 for median price error). A param of 450 has the highest annualized returns (0.092%) with median price error only ~3.3% higher (0.0245 vs 0.0237).

Yep, if you fit exactly to the simulations assuming the data is perfect and the world behaves exactly as in the past, then these would be the right conclusions. If you realize data is imperfect, the future is not exactly as the past, and that increasing A increases risk, you reach quite different conclusions.

An A param of 450 will also result in the highest volumes as shown in the simulations by @nagaking.

I’ve already pointed out there is a lot of noise around the peak for returns. The same is true for the volumes graph. Overfitting without prudent consideration of the increased risk is not wise.

Increasing A from 100 to 150 does seem to lead to some tangible benefits for LPs, so may be worth considering. Raising to 450 is reckless, although given what has been communicated by your team, I can understand why you would want to do this.

After consulting with my team, I have an additional perspective to share. I work with Concave, as a Partnerships Team Lead.

Today, I am speaking on behalf of Concave which would benefit from the A Param increase, since our protocol has a sizable eight digit position in the DOLA+3CRV pool. We are aware of larger wallets that are potentially interested in this Pool, and we believe an increase would be mutually beneficial since there would be less slippage from entering or exiting larger positions. With the A Param at 100, there is more friction when trying to exit and enter due to the slippage that would occur. The DOLA-3POOL, we believe, can be much stronger with a 450 A param due to a stronger peg despite slight pool imbalances. As far as the increased gamma to LPs is concerned, we believe the tradeoff for decreased trade slippage, and the potential growth in TVL of the pool is worth it.

Hi - I lead the risk team at Inverse and want to thank everyone for creating a constructive discussion around DOLA on Curve. The feedback has been excellent and we have decided to pause the current proposal and come back soon with an improved proposal that includes a lower A param.