As the market became more sane, I propose to change monetary policies for LlamaLend on Ethereum once again. However, this time I attach a spreadsheet so that everyone can look at the reason for the numbers and try.

Proposed changes:

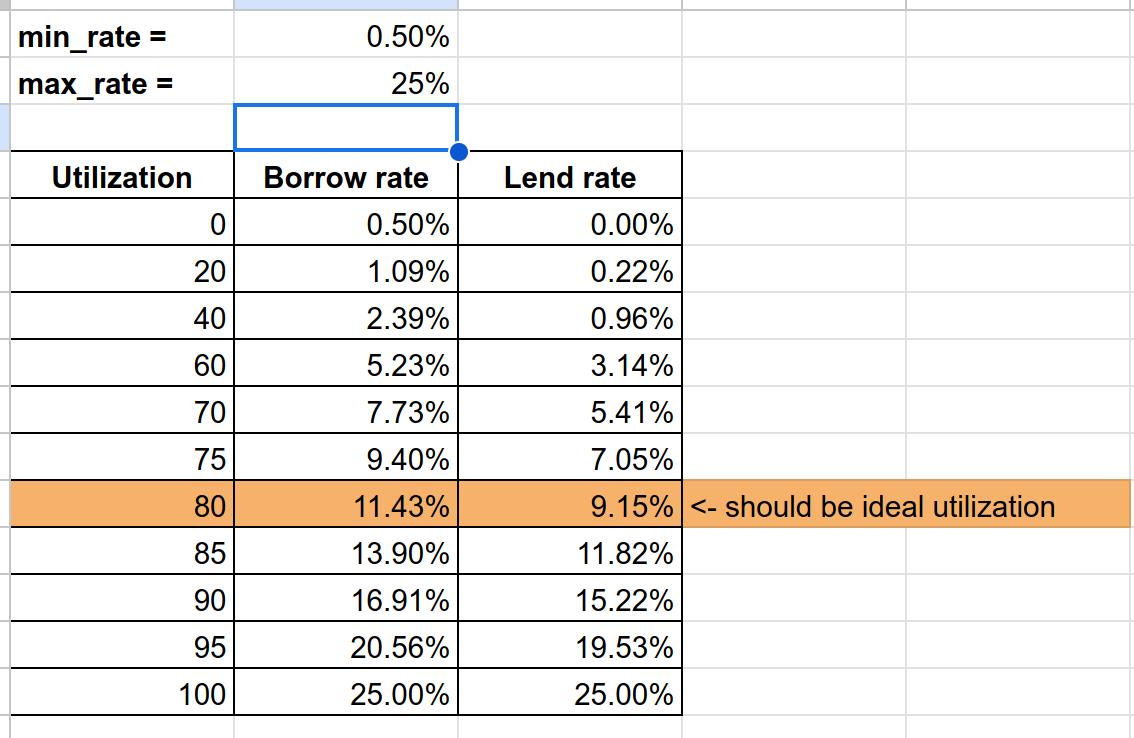

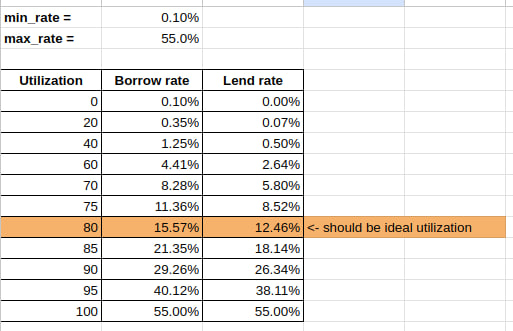

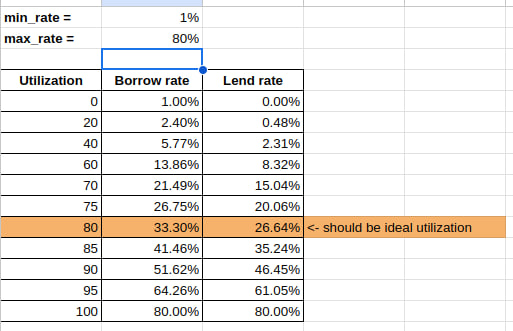

WETH and tBTC markets: min_rate=0.5%, max_rate=25%

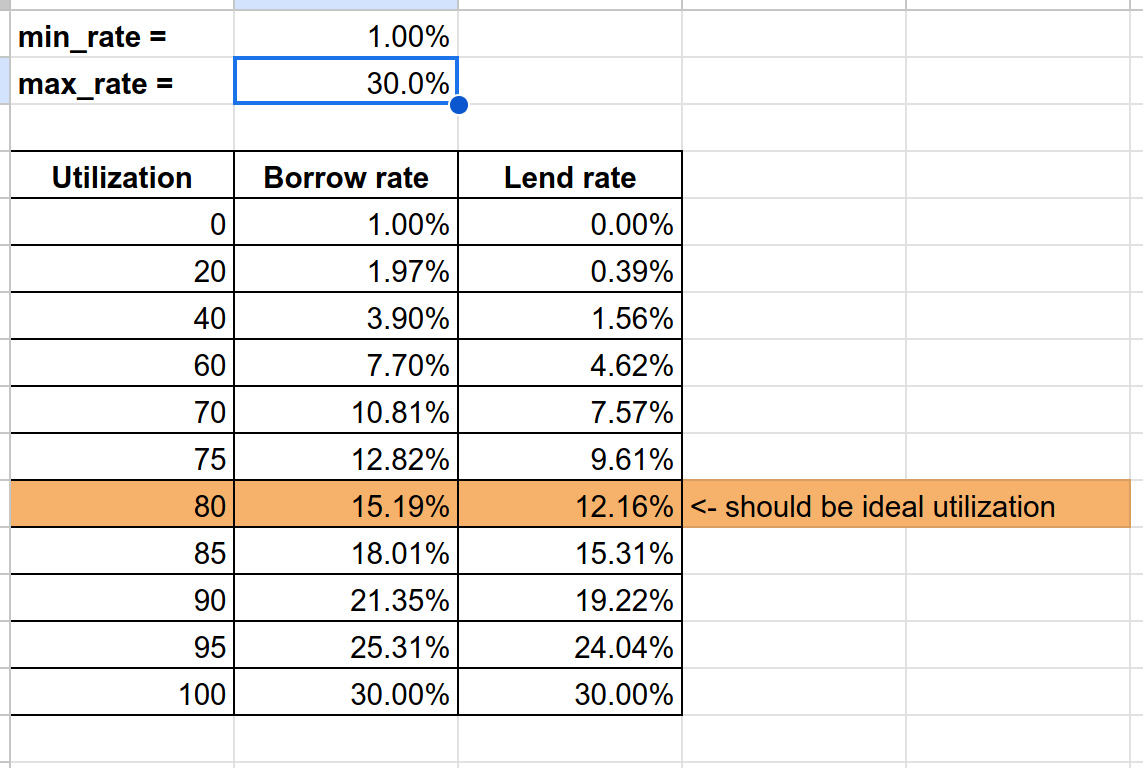

wstETH: min_rate=1%, max_rate=30%

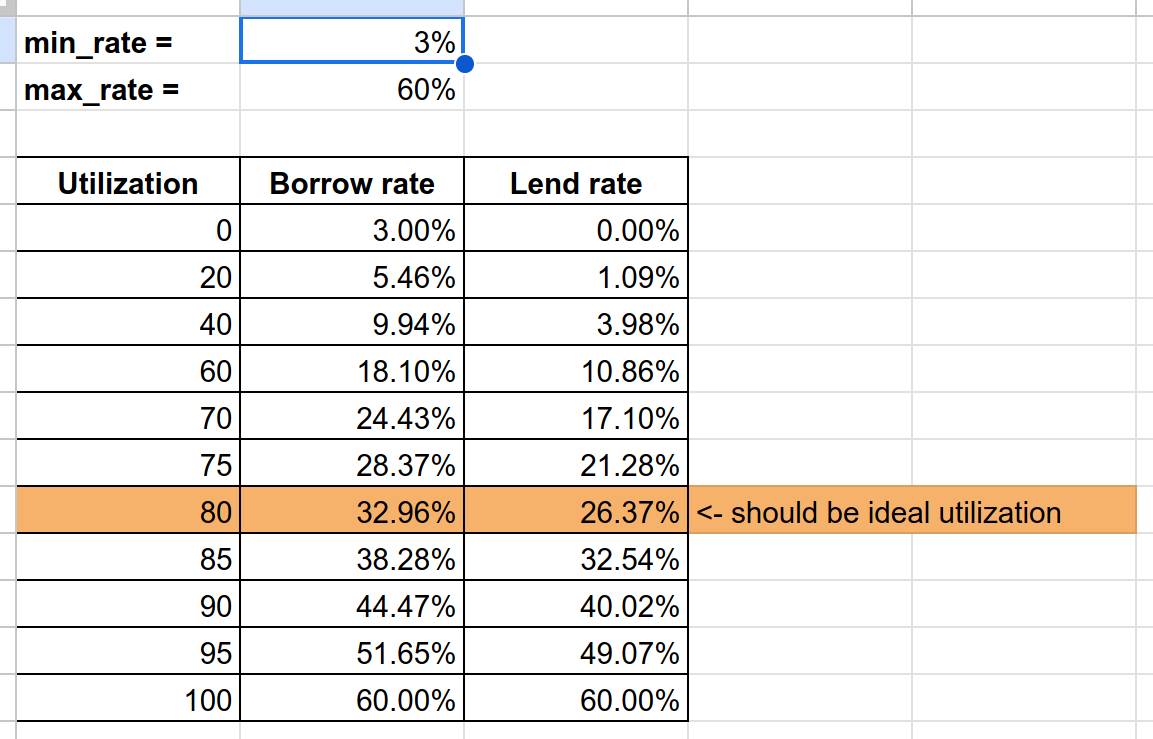

CRV: min_rate=3%, max_rate=60%

Reasoning

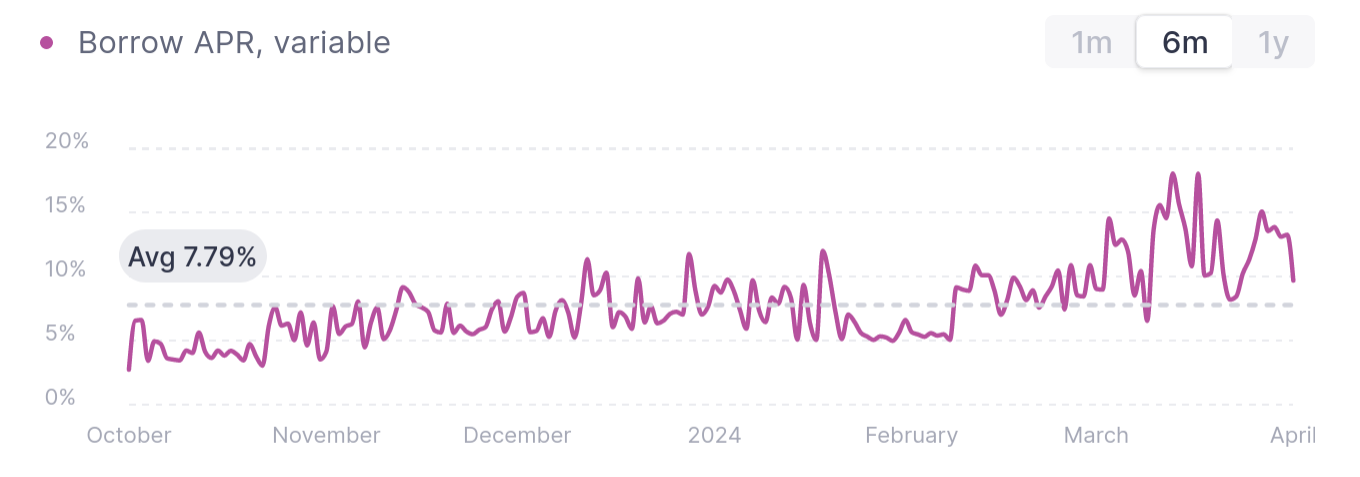

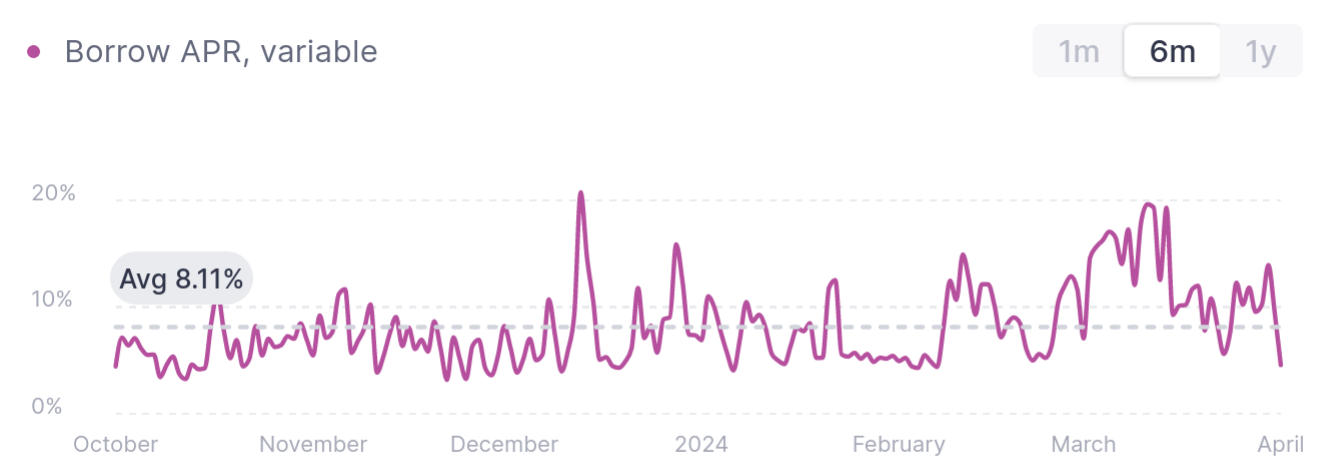

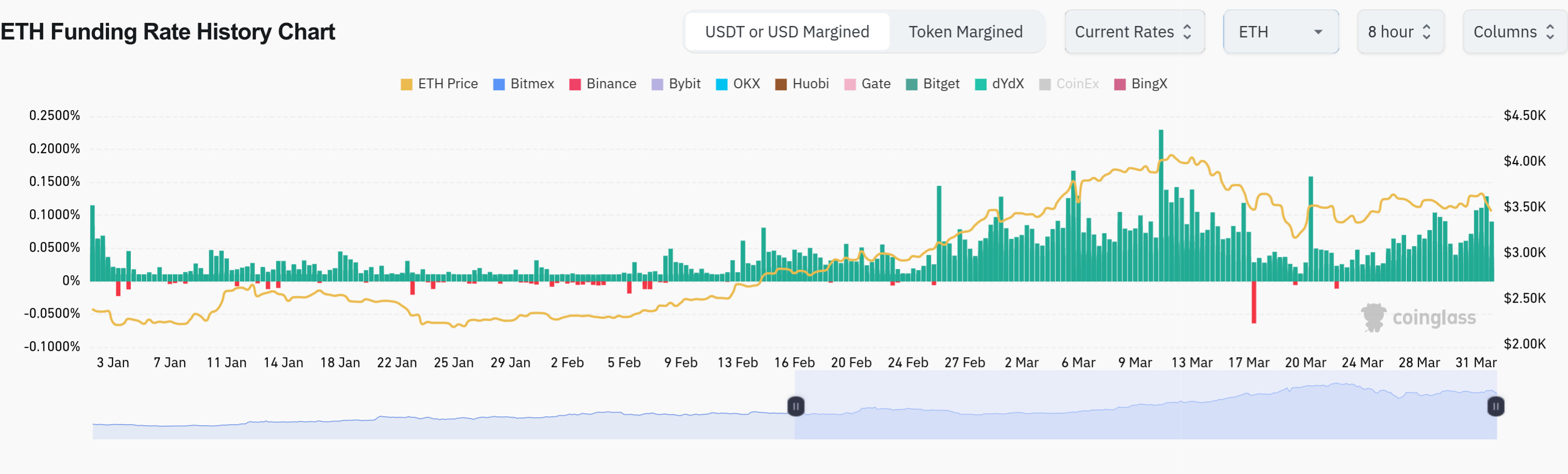

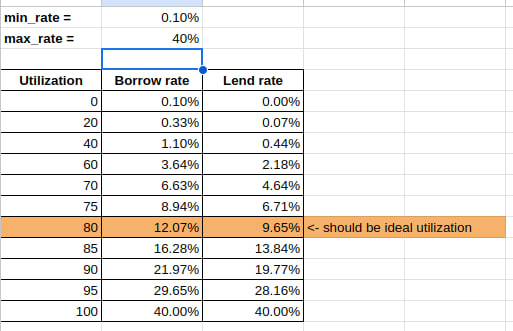

Goal is to make borrow rate at 80% utilization to be approximately equal to current market rates. If rates change slightly (say, ± factor of 2) - same monetary policy should still work ok.

This model looks at other lend/borrow rates. Should we be doing that, or rather looking at perp funding rates? Discussions are welcome

Model

A simple “model” is made in a form of a spreadsheet. For convenience, I attach screenshots.

Offer two separate markets for Perp/Borrowers; that they do not fragment liquidity internally, how Sturdy or Fluid works; where the LlamaLend-Perp parameters are competitive for the Perp market; and LlamaLend-LM is for borrowers.

What do you think? Is it technically possible?

Yes, can make several markets where one of them can easily run out of liquidity - no problem. Question is - who will at all lend out money to markets with lower rates?

Lower rates (for the LP) will not be a problem of one market or another (Perp-Lens market), but of the liquidity vaults, which is where the LP sends its assets.

Each vault should allow “Products” across the full range of lending market and perp market, e.g. LEND-WETH LEND-WBTC PERP-WETH. The liquidity provider will choose the vault that suits them; The configuration of each vault (liquidity layer) must consider 1) the products to which it provides liquidity 2) its distribution. Possibly a vault provides both markets (Perp and Lens) only for WETH and WBTC e.g. and if an LP considers the best option it will go for this vault; Then the “product” layer will take this liquidity according to the parameters configured for each market (Perp - Lens).

I think Morpho and Sturdy have some of these functions, although limited to the lending market; Maybe LlamaRisk can guide us with this.

The lowest rates, in either of the 2 markets; will attract demand from borrowers/traders; and if the vault beneficiary of this demand combines both markets this will be an advantage for all liquidity; in case the vault only provides liquidity to Lend-market for example, and we see lower rates; Possibly LPs migrate to other vaults with higher APY; and the rates that the counterparty of this deficient vault is paying increase due to the drop in liquidity.

My point is, why not cover both markets?

Because you cannot be competitive in 2 different markets if we are going to use the same parameters for all liquidity.

The solution I find: today we see a unification of liquidity possible; which can be directed to the different “products” and parameter configuration, which contemplate all the necessary points to differentiate Perp/Lens; optimal utilization and design of the rate curve, maximum utilization, supply limit, etc.; for each market.

In this way, the TVL of crvUSD will be distributed by liquidity Vaults (Base layer), with a liquidity provision according to parameters for Perp markets - Lending markets (Product layer)

I am not sure if migrating this design to a single liquidity vault, which concentrates all the TVL, can be a better alternative; There would be simplification in the UX, possibly an improvement in the overall performance of the protocol, gas efficiency and fewer points of failure, although greater concentration.

Thinking about it, a single deposit Vault; It would allow representing the crvUSD stake (similar to DSR); feeding the entire layer of products, it would possibly bring high profit and diversity to maintain demand not linked to a single business; looks like a great product.

Let the season of: “Wen CurvePerp” and “Wen ScrvUSD” begin